Understanding your credit rating

Read our explanations and advice on how to manage your credit rating.

In summary:

- Your credit report is a key tool that lenders review to decide whether or not to approve you for a loan.

- It provides a combined overview of your credit score and credit rating.

- You can check, improve, or correct your credit report through Equifax and TransUnion to ensure it accurately reflects your financial habits.

Understanding and managing your credit report is a crucial step toward maintaining good financial health. This tool plays an important role in decisions made by lenders, financial institutions, landlords, and sometimes even employers. It reflects your credit management habits and can influence your ability to get a loan, a credit card, housing, or even the terms you are offered, such as interest rates. By understanding the elements that make up your report, including your credit score and rating, you will be better equipped to identify errors, strengthen your report, and achieve both your short term and long term financial goals.

Explore our explanations and tips to understand what a credit report is and how the 2 credit reporting agencies, Equifax and TransUnion, manage your file.

Your credit report

Your credit score

What is a credit report?

A credit report is a document that brings together various details about your financial situation, including some of your personal information. It is used to identify you, assess your level of debt, and most importantly, determine whether you repay your debts responsibly. A credit report is mainly used by different types of organizations to evaluate your financial reliability before offering you a product or service.

What does a credit report contain?

A credit report includes your personal information (name, date of birth, addresses, current employer), as well as a list of your past and current credit accounts, such as credit cards, loans, and lines of credit. For each account, it shows the amount borrowed, the balance owing, your payment history (on time or late), and your credit rating (for example: R1, R2, R9). The report also lists recent credit inquiries, public records related to your financial standing (such as a bankruptcy), and any lender comments, if applicable. Finally, the credit report includes your credit score: a number between 300 and 900 that sums up your financial reliability and gives lenders a quick reference to assess the risk of lending to you.

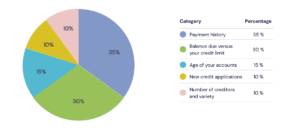

5 factors that influence your credit score

Based on the information in your credit report and the ratings assigned by your creditors, the credit bureaus give you a score that typically ranges from 300 to 900. A high score indicates a long and positive credit history. You can find more detailed information about these 5 factors that determine your credit score.

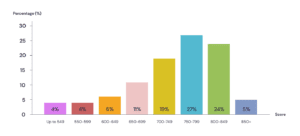

Here is the national credit score distribution for individuals with a credit file at Equifax Canada:

(source: Equifax.ca)

Explanation of credit ratings (R0 to R9)

| R0 | File is too new to rate. Credit is approved but not yet used. |

| R1 | Pays within 30 days. |

| R2 | Pays within 31 to 60 days. |

| R3 | Pays within 61 to 90 days. |

| R4 | Pays within 91 to 120 days. |

| R5 | Account is more than 120 days overdue but not yet rated «9». |

| R7 | Debts paid at the end of a debt consolidation loan, or voluntary deposit at Court, or any other similar arrangement, such as a consumer proposal. |

| R8 | Repossession. |

| R9 | Bad debt; placed for collection; moved with no forwarding address; bankruptcy. |

«R» that precedes the number means that it is a revolving credit, such as a credit card or a personal loan. If the debt is an installment sale, like a car loan, the letter will be «I». Additionally, for an open line of credit, the letter «O» is used, and «M» is used for a mortgage.

How is your credit report created?

A credit report is automatically created as soon as you start using credit. This usually happens when you open a credit account, such as a credit card (bank or store), a student loan, a car loan, or a line of credit. Opening certain service accounts, such as those related to phone, internet, or TV services, can also contribute to the creation of your credit report.

There is no need to request it yourself, as the report is created automatically when a lender or service provider reports activity to one of the credit bureaus. If you have never used credit, you may not have a credit report, or it may contain only a limited history, which can make accessing credit more difficult.

Who can access your credit report?

Your credit report can be accessed by certain authorized organizations, with your written consent in most cases. This includes financial institutions, landlords, service providers (phone, internet, electricity), certain employers, insurers, and, in some cases, government or legal authorities. These checks are used to evaluate your creditworthiness and financial reliability. It is important to note that your report is not accessible to people around you (friends, family, or current employer), and your written authorization is still required in almost all situations.

To obtain your credit report

Under the law, you have the right to request a copy of your credit report and your credit score. You can obtain them for free from Equifax by becoming a member at Equifax.ca.

In addition, to obtain your free credit report from TransUnion, you must become a member at TransUnion.ca.

Free access now includes your credit score, which provides an overall assessment of your credit file.

To check your credit report

Once you have received your Equifax and TransUnion credit reports, we invite you to verify the accuracy of the information listed in your credit reports. You will find examples of the information that should be visible following a bankruptcy and a consumer proposal.

To correct your credit report

Under the law, credit bureaus are required to provide accurate information. Therefore, if you notice an error, they must correct it if you provide supporting evidence.

| Equifax | TransUnion |

| You must first complete the Consumer credit file update form.

However, if you are unable to fill out and submit the form online, we recommend contacting them:

Here is Equifax’s website address. First, they will review and consider the information you provided regarding the dispute. If the initial review does not resolve the issue, they will continue their investigation. This includes contacting the reporter who is disputing the information to review the details. After the investigation, they will present the results to you. Based on those results, they may make changes to your credit file. If the disputed information is found to be accurate, no correction will be made. They will send you a copy of your updated credit report if any changes are made following the dispute resolution process. They will also send a revised copy of your report to any company that requested your file within the 60 days prior to the correction. In some cases, this period may exceed 60 days. |

You must first complete the investigation request form.

However, if you are unable to fill out and submit the form online, we recommend contacting them:

Here is TransUnion’s website address. |

If you have any questions about your credit file, feel free to contact one of our financial restructuring advisors. It’s quick, free, and confidential.

Your questions

Does checking my credit score lower it?

No. Checking your own credit report has no impact on your credit score. On the contrary, it helps you better understand the effect of your financial decisions.

However, your credit is reviewed each time you apply for a loan with a lender, and this can influence your credit score.

It is recommended to review your credit report every 6 months to monitor changes and quickly correct any errors.

How long does it take to improve your credit score after a late payment?

A late payment can affect your credit score for up to 6 years, and it may take several years to fully recover.

We invite you to read our “5 tips to increase your credit score.”

I have a poor credit report, what are the consequences?

A poor credit report can have consequences on your day-to-day life. We invite you to read our article on the consequences of a poor credit report to learn more.

Is it possible to improve your credit score quickly?

Improving a credit score can take anywhere from 3 to 12 months, depending on each person’s individual situation. We invite you to consult our “5 tips to increase your credit score” to help guide you through this process.

What are the risks of a high debt ratio?

A high debt ratio can seriously affect your financial health and well-being. In the blog “What are the risks of a high debt ratio?“, we explain what is a debt ratio, how to calculate it and we explain how to interpret the results. Finally, we review in detail the risks associated with a high ratio. Being well informed on this subject will help you be better prepared to take the necessary measures to avoid falling into a debt spiral.

What is considered a good credit score in Canada?

We invite you to consult “What is a good credit score”, which will help you determine whether your credit score is poor, fair, good, very good, or excellent—and better understand what that means for your financial situation.

What is the difference between a credit report, credit rating, and credit score?

A credit report contains your complete financial history, including your debts, loans, credit cards, and payment habits. It has two components: the credit rating and the credit score.

The credit rating reflects, each month, the information your creditors provide about your repayment habits. It is shown as a rating from R0 to R9, based on how punctual your payments are.

The credit score, on the other hand, is a number between 300 and 900 that summarizes this information to assess your creditworthiness. It allows lenders to estimate the risk of lending you money, much like a grade reflecting your past financial management. This score is calculated using the data in your credit report.

Our debt solutions

Based on your situation and needs, there are different solutions that can help you regain your financial stability.

Debt Consolidation

Find out how to merge all your payments into one monthly installment and keep your credit score intact.

Consumer Proposal

Discover how to offer your creditors a lower settlement based on your ability to repay.

Personal Bankruptcy

Discover how personal bankruptcy can put an end to your financial difficulties and debt problems.