How to create a simple and effective budget?

In summary:

- A budget should be realistic, flexible, and reviewed regularly, while taking clear financial goals into account.

- It is essential to include all income and expenses and to classify them by category in order to analyze the results and adjust the budget if necessary.

- Saving is indispensable to deal with unexpected events and to achieve short, medium, and long-term goals.

Why is creating a budget essential?

Creating a budget is important because it helps you better control your finances, avoid excessive debt, and make informed decisions. It allows you to see where your money is going, anticipate unexpected expenses, and reach your financial goals more easily. A well-structured personal budget reduces money-related stress and promotes better financial security in both the short and long term.

To help you create a personal or family budget, feel free to consult our online budgeting tool, which can be downloaded and adjusted over time.

The 5 steps to creating a budget

Creating a budget may seem complex at first, but by following a simple and structured method, it becomes a powerful tool for managing your finances. Before you begin, it’s important to gather all the necessary information, such as your income, bills, and regular expenses.

1. List all your income

Including all sources of income is a fundamental step in creating a budget. It is important to identify every source of income, whether regular or occasional, such as salary, self-employment income, benefits, tax credits (GST, solidarity tax credit, etc.), pensions, or other cash inflows. To get a realistic picture, it is recommended to use net amounts and to rely on averages when income fluctuates. This step allows you to know exactly how much money is available and to create a budget that reflects your true financial capacity.

2. List your expenses

Next, to obtain a complete and realistic picture of your budget, it is essential to list all your expenses and classify them properly by type. Be sure to include savings as well as an amount for small pleasures and leisure activities. These elements are important to maintain financial balance and avoid financial stress.

A budget includes 3 types of expenses:

- Fixed expenses

These expenses are easy to identify because they recur every month, are known in advance, and vary very little from month to month (e.g., rent, car payments, insurance, internet, cellphone, TV subscriptions, etc.). - Variable expenses

These are expenses that occur regularly but vary from month to month (e.g., groceries, personal spending, clothing). Unless these expenses are tracked meticulously for at least two months, it is difficult to determine them precisely. They are first estimated, then adjusted based on actual spending. - Irregular expenses

These expenses can occur at any time during the year and the amount is often unknown in advance (e.g., car repairs, home maintenance, tires, etc.). They should still be estimated ahead of time, and money should be set aside each month to build a dedicated fund.

3. Classify your expenses into budget categories

Classifying your expenses into budget categories helps you better understand where your money goes and ensures a balance between your needs, obligations, and financial goals. Ideally, the main budget categories should be allocated as follows:

- Housing (including rent, mortgage, property taxes, heating, and electricity): between 25% and 30%

- Transportation costs: maximum 20%

- Food: between 15% and 18%

- Savings: between 5% and 10%

- Debt: maximum 15% (monthly payments)

- Leisure: allocate a small amount to avoid “budget fatigue” and support long-term success

- There are also different methods for structuring your budget:

The 50/30/20 method suggests allocating 50% of your income to essential needs, 30% to discretionary spending, and 20% to savings and debt repayment. This simple approach is ideal for achieving good financial balance.

Zero-based budgeting, on the other hand, involves assigning a specific purpose to every dollar of income so that total income minus expenses equals zero. Every dollar is planned, whether for expenses, savings, or leisure, allowing for tighter financial control.

These methods can be adapted to your financial situation, goals, and lifestyle.

4. Analyze your results

Negative result: Once your budget is established and your expenses are compared to your income, it is important to analyze the outcome. If your financial balance is negative, it means your expenses exceed your income. In this case, you need to reduce certain expenses, such as leisure activities, non-essential purchases, or variable costs, in order to restore balance. You may also consider renegotiating some fixed expenses, such as insurance or utility services, to reduce overall monthly costs. Money doesn’t fall from the sky: a budget deficit is covered either by savings or by access to credit. In both cases, this situation is not desirable, especially if it continues over time.

Positive result: Conversely, if your budget shows a surplus, take advantage of it to strengthen your financial security. For example, you can pay down debt faster, increase your savings, or invest to prepare for future projects. The key is to use this surplus thoughtfully so it serves your short-, medium-, and long-term goals rather than being spent without a plan. A well-managed surplus is a powerful lever for improving your financial health.

Ideally, it is recommended to save at least 10% of your net income to create funds suited to your needs:

- Short term: a cash-flow fund equal to one month of expenses to avoid using credit for everyday spending.

- Medium term: an emergency fund equal to approximately 3 months of salary to deal with illness, job loss, or unexpected repairs without going into debt.

- Long term: a retirement fund using tools such as an RRSP, TFSA, or RESP.

“Slow and steady wins the race”: have a small amount deducted from each paycheck. You’ll learn to live without that money and save without even noticing it.

5. Track your budget and be realistic

For your budget to remain effective, it is essential to review it regularly to ensure your expenses align with your projections. Don’t hesitate to adjust your budget if your income or needs change. It’s important to be disciplined, but not overly strict: a budget that is too restrictive with unrealistic goals can lead to frustration and ”financial stress”, increasing the risk of giving up. In short, a realistic and flexible budget is the key to staying in control of your finances while maintaining a good quality of life.

You can also involve your children or dependents in creating the family budget, particularly for the sections that concern them (allowance, vacations, leisure activities, sports, school supplies, etc.). This exercise will benefit them in the long run and may help them become more aware that money doesn’t grow on trees!

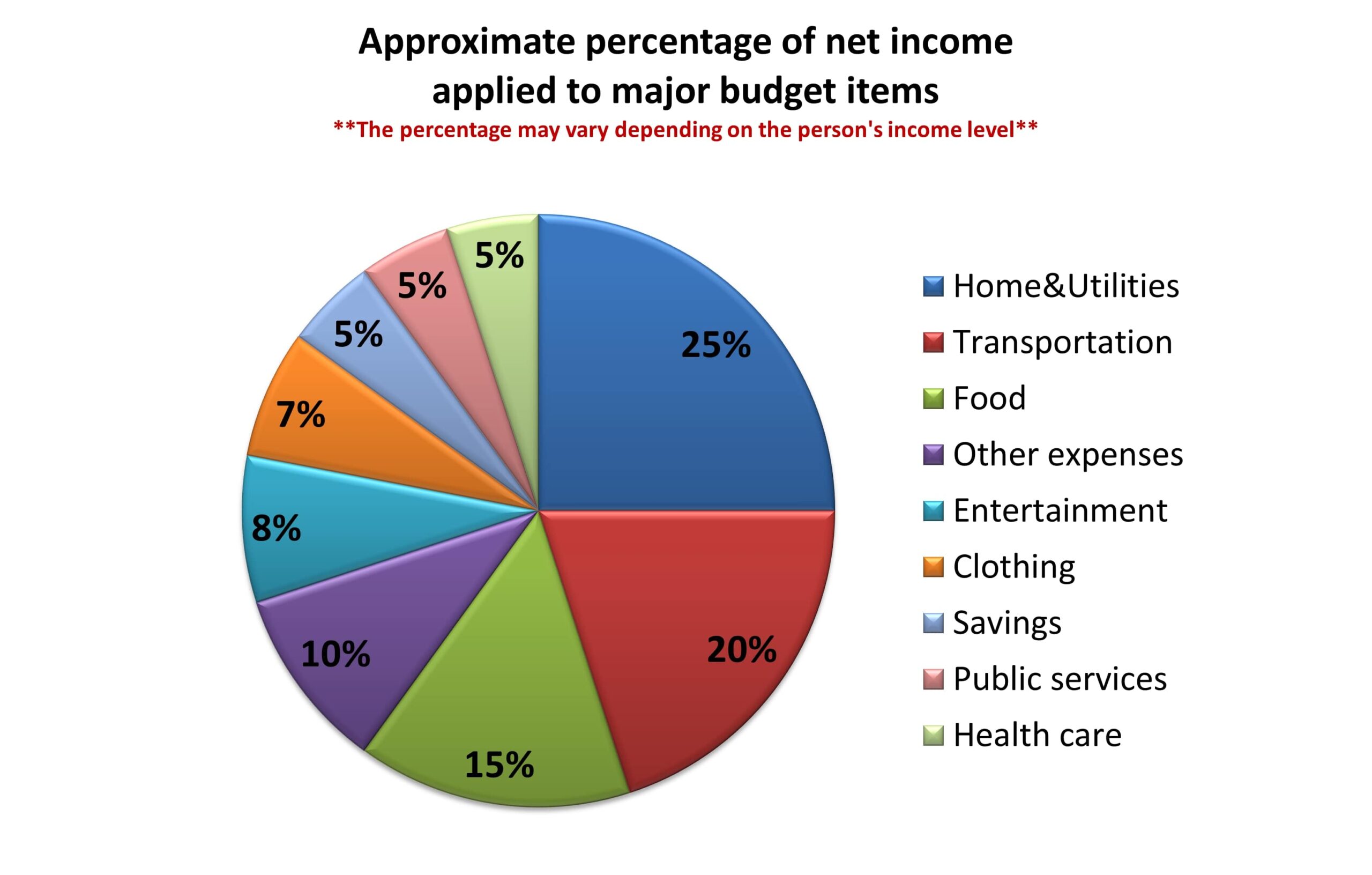

Budget example

Here is an example of a “typical” budget allocation:

Housing: 25% of income, including rent or mortgage

Transportation: 20%, covering fuel, insurance, and vehicle maintenance or public transit

Food: 15%, for groceries and dining out

Other expenses: 10%, including subscriptions, miscellaneous fees, and unexpected costs

Leisure and vacations: 8%, to maintain balance and avoid budget fatigue

Clothing: 7%, for clothing and footwear

Savings: 5%, to build an emergency fund and prepare for future projects

Utilities: 5%, including electricity, heating, and water

Health care: 5%, for medications, insurance, and medical appointments

*Note: These percentages are approximate and may vary depending on household size, lifestyle habits, and income level.

In summary, creating a budget is an essential tool for better managing your finances, achieving your goals, and avoiding the stress of unexpected expenses. It allows you to take control of your money and plan your projects with peace of mind. To maximize the effectiveness of your budget, it is important to avoid common budgeting mistakes that can compromise your financial balance.

Finally, for personalized advice and to explore strategies tailored to your situation, feel free to book an appointment with one of our experts, free of charge and in complete confidentiality.

Happy budgeting!

By Pierre Fortin

Jean Fortin & Associés

Personal Finance Advisor

Licensed Insolvency Trustee

When debt challenges become overwhelming, you don’t have to face them alone. Our advisors are ready to guide you (free, no-obligation consultation).

See also...

Financial Health Checkup

The perfect tool to get a quick picture of your financial situation.

Online Budget

Create a budget to track your spending and successfully manage your financial priorities.

Properly planning important expenses

Our advice on how to plan for major expenses while avoiding debt.