What is the debt ratio?

In summary:

- The debt ratio is the tool banks use to determine whether you are able to repay the loan you are applying for.

- This very simple formula calculates the weight of your debts and housing costs relative to your income. In a way, it acts as a thermometer of your borrowing capacity.

- A debt to income ratio below 30% is excellent, while anything above 40% is a red flag.

Having a clear overall view of your finances is essential for making informed decisions, whether borrowing, investing, or simply managing your budget more effectively. Among the key indicators to monitor, the debt ratio, which represents the portion of your income devoted to repaying your debts, quickly shows whether your situation is healthy or needs adjustment.

How to calculate your debt to income ratio?

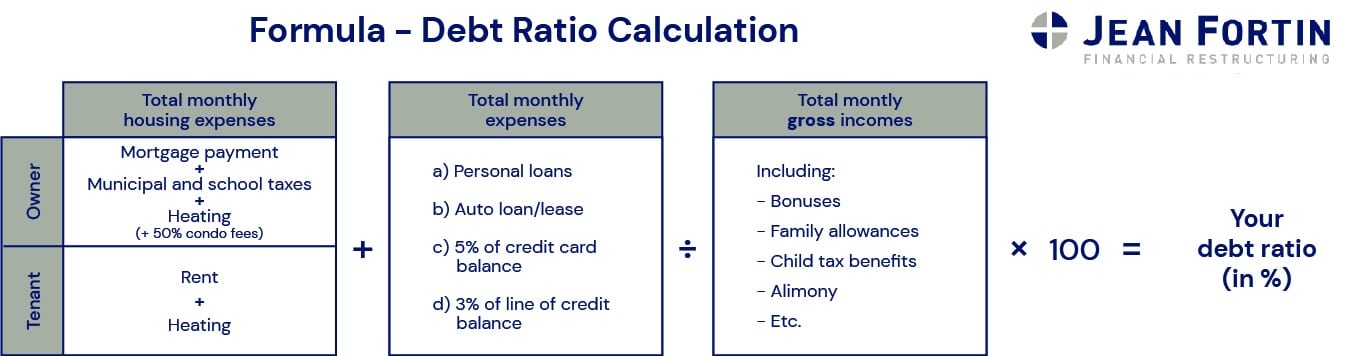

To determine your level of indebtedness, you will need the following amounts:

- Your gross salary

- Child support, pensions, family allowances, and other secondary income

- Your housing costs (rent or mortgage, condo fees, heating, etc.)

- Your debts (personal loans, car loans or leases, lines of credit, credit cards, etc.)

Here is the debt ratio formula in more detail:

To simplify calculating your debt to income ratio, Jean Fortin professionals have created an online tool that is fast, secure, and anonymous. You are encouraged to use it as often as you like.

What does your debt ratio result mean?

After determining your debt level using our debt ratio calculator, you will receive one of several possible results along with advice.

| RESULTS | YOUR DEBT RATIO |

| Excellent | is less than 30% |

| Very good | is between 30 and 35% |

| To monitor | is between 35 and 40% |

| Help needed | is over 40% |

“If the result exceeds 40%, it indicates a problem that needs to be addressed, without necessarily meaning a bankruptcy situation. The most dangerous thing is being unaware of it or refusing to face reality,” concludes Pierre Fortin, President and Licensed Insolvency Trustee.

Why monitor your debt ratio?

As insolvency professionals, we find that our clients often tell us that over-indebtedness can can develop in a subtle and gradual way. It is therefore essential to recognize early warning signs and act quickly, rather than waiting for a call from a collection agency or credit refusal.

Moreover, the phenomenon is far from marginal: Canada ranks among the G7 countries where households are the most indebted, and the level of household debt (not to be confused with the debt ratio) continues to rise1. According to Statistics Canada data from September 2025, household debt remains very high, and Canadians spend on average about $1.75 to $1.80 for every dollar of disposable income2. Why is it so high? Mainly because housing prices in Canada are extremely high compared to those of our neighbors to the south, for example. High property values often mean large mortgage balances, which in turn contribute to high levels of debt. Some will argue that a mortgage is “good debt” because it allows a person to own an asset that will appreciate over time, but the fact remains that a large mortgage balance places a heavy burden on a household budget and therefore reduces a person’s ability to cover other essential expenses. Often, a house can become a financial burden and force homeowners to rely on credit cards or lines of credit just to make ends meet. These statistics illustrate how easy it is to lose control without even realizing it.

“Setting aside major life events such as divorce or job loss, we observe that, in many cases, people become aware of their financial situation too late. They did not have a budget and were unaware of both the balance and the interest rate on their credit card,” continues Pierre Fortin.

What are the risks of a high debt ratio?

A high level of debt can have several significant consequences on your financial health and quality of life, including:

- A major budget imbalance and the stress that comes with it;

- Reduced ability to save, invest, and achieve your financial goals;

- Lower credit eligibility (or access to more expensive credit due to higher interest rates), particularly for major projects such as buying a home.

The higher your debt ratio, the higher the interest rates on potential loans may be, as financial institutions may consider you a higher-risk borrower. It is often at this stage that the people we meet wish they had consulted us earlier.

Also check out our tips to help you improve your debt ratio if you find it is too high after receiving your results.

The benefits of calculating your debt to income ratio

First, this is the tool all financial institutions use to measure your level of indebtedness. It helps determine whether you can handle the loan you wish to obtain. Its real value lies in the fact that it is universal, simple, and allows you to track the progress of your situation over time. You can always see where you stand and make adjustments if needed.

What are the limitations of the debt ratio calculator?

Unfortunately, this tool has 2 major limitations to keep in mind:

- It does not take into account your family situation or personal expenses beyond housing costs. For example, a single person earning $100,000 does not have the same financial obligations as a family with 2 children and 2 parents each earning $50,000.

- It does not consider your lifestyle habits. Do you like to travel, or do you have higher-than-average expenses for transportation, food, etc.?

Therefore, relying solely on the debt ratio cannot guarantee a strong financial situation. Our experts also recommend creating a budget that accounts for all your expenses and provides a more accurate picture of your reality. While this requires more time than simply calculating your debt to income ratio, investing time in both will give you a clearer understanding of your finances.

Who should you consult when your debt level is high?

Even today, we too often find that consulting a trustee can be intimidating. However, they are best positioned to help you restore your financial situation and manage rising debt levels. Bankruptcy is never the first option, there are other solutions, and the trustee will take the time to review and explain them.

Rest assured, during your free informational meeting, the Licensed Insolvency Trustee will not judge you. They will listen, answer your questions, ease your concerns, and support you in reorganizing and planning your finances.

This is what has set Jean Fortin apart since 1984: a human, non-judgmental approach focused on listening and providing concrete solutions tailored to your reality. Their team emphasizes transparency and takes the time to properly inform you so you can make sound decisions and regain control of your financial situation.

If you have any questions or if your financial situation concerns you, please don’t hesitate to contact us.

By Pierre Fortin

Jean Fortin & Associés

Personal Finance Advisor

Authorized Insolvency Trustee

1 https://www.conseiller.ca/nouvelles/les-menages-canadiens-au-sommet-de-lendettement/

2 https://www.statcan.gc.ca/o1/fr/plus/8747-nos-finances-mieux-les-comprendre-et-en-parler

When debt challenges become overwhelming, you don’t have to face them alone. Our advisors are ready to guide you (free, no-obligation consultation).