How much does a bankruptcy cost?

Discover the factors that determine the cost of a bankruptcy.

The cost of bankruptcy depends on 3 factors:

1. Is it your first bankruptcy?

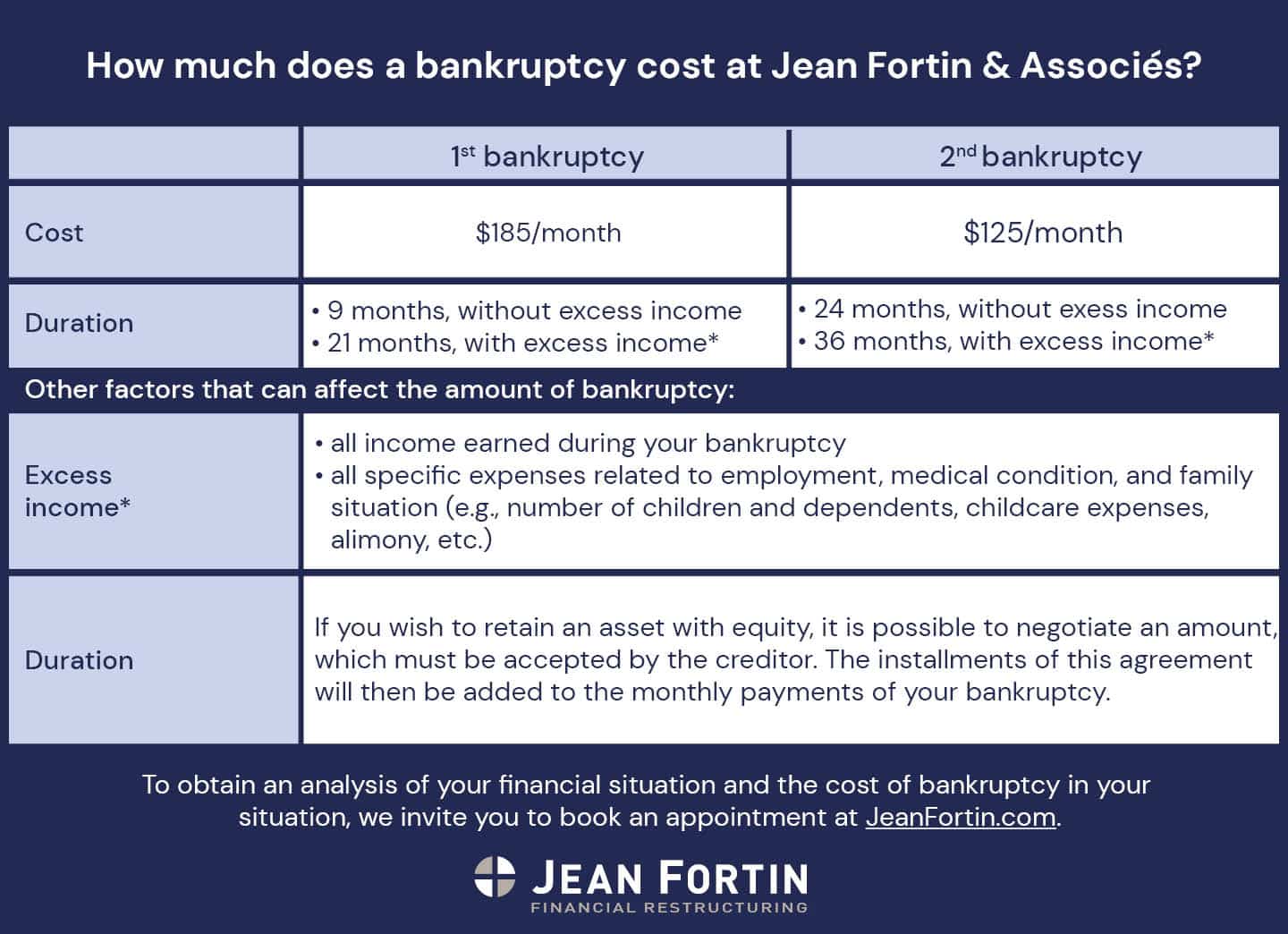

If this is your 1st bankruptcy, you’ll need to make monthly payments of $185 per month for 9 months in the absence of “excess income” (see point 2).

If this is your 2nd bankruptcy, the monthly payment will be $125 per month for 24 months in the absence of excess income.

Note that the price may be higher in other trustee firms as each can establish its own minimum monthly amount.

2. Do you have “excess income”?

To determine whether you have excess income or not, your advisor must consider:

- all income earned during your bankruptcy; and

- all specific expenses related to your employment, medical condition, and family situation (e.g., number of children and other dependents, childcare expenses, alimony, etc.).

Once all these amounts are accounted for, your advisor will explain the calculation dictated by the federal government and the resulting outcome.

If you have excess income at the time of filing for bankruptcy or during the process, your bankruptcy could be extended for an additional 12 months. Thus, a 1st-time bankruptcy could last a total of 21 months and a 2nd bankruptcy, 36 months.

Note that if the mandatory payments or the duration of your bankruptcy are not suitable for you, you have the option, during your bankruptcy, to extend the duration of your bankruptcy or to convert it into a consumer proposal. In the event of a proposal, the trustee would present an offer to your creditors, and if a majority approves, your proposal would replace the bankruptcy.

3. Do you own assets?

When an asset has a value that exceeds the balance of the secured loan (e.g., mortgage, auto loan, etc.), the difference is called the equity.

If you file for bankruptcy and wish to keep your house, for example, any equity in it, would have to be dealt with by a payment agreement (over a few months or years) with the trustee. The idea is to make sure that the creditors are compensated for the equity that you want to keep. Of course, any agreement must be approved by the creditors.

In this case, the payments are added to the monthly payments you have to make but they can be made over a longer period than the duration of the bankruptcy.

Finally, it is important to note that federal income tax returns (but not the provincial returns) as well as GST credits (up to a threshold established by the law) up to the year of bankruptcy, are considered as seizable assets. Also, any amount you may receive before or during your bankruptcy as inheritance or lottery winnings will be part of your estate and be divided amongst the creditors.

At your 1st meeting, your advisor will analyze your financial situation and inform you of all the details that are specific to your situation.

Consultations are free, confidential, and without obligation.

By Pierre Fortin

Jean Fortin & Associés

Personal Finance Advisor

Licensed Insolvency Trustee

When debt challenges become overwhelming, you don’t have to face them alone. Our advisors are ready to guide you (free, no-obligation consultation).